Kian-Ping Lim

Financial Economist

Financial crisis and stock market efficiency: Empirical evidence from Asian countries*

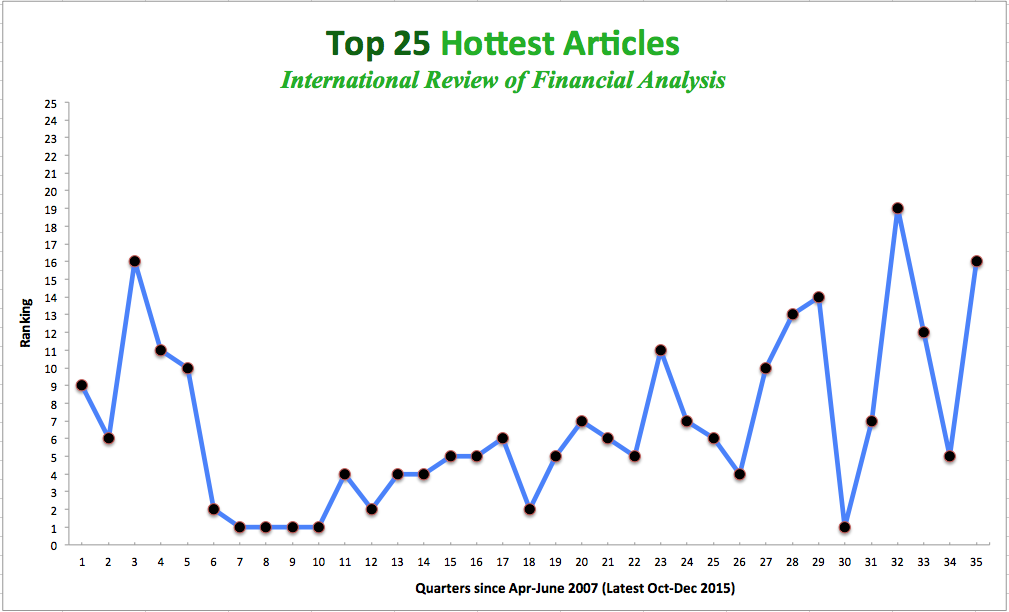

Top 25 Hottest Articles for 35 Consecutive Quarters!

Abstract

This paper empirically investigates the effects of the 1997 financial crisis on the efficiency of eight Asian stock markets, applying the rolling bicorrelation test statistics for the three sub-periods of pre-crisis, crisis, and post-crisis. On a country-by-country basis, the results demonstrate that the crisis adversely affected the efficiency of most Asian stock markets, with Hong Kong being the hardest hit, followed by the Philippines, Malaysia, Singapore, Thailand and Korea. However, most of these markets recovered in the post-crisis period in terms of improved market efficiency. Given that the evidence of nonlinear serial dependencies indicates equilibrium deviation resulted from external shocks, the present findings of higher inefficiency during the crisis are not surprising as in the chaotic financial environment at that time, investors would overreact not only to local news, but also to news originating in the other markets, especially when the news events were adverse.

Keywords

Market efficiency; Asian crisis; Stock market; Nonlinear serial dependence; Bicorrelation